Accounting for Small Businesses: A Comprehensive Guide to Financial Management

This type of statement provides a snapshot of a small business’s financial health at a specific point in time. Bookkeepers can view the company’s assets and liability figures at a glance. Your business should implement efficient record-keeping policies and a sound financial strategy to avoid this situation. You’ll want to gather and record all your transactions, usually weekly, but you can do this daily or bi-weekly, depending on your volume. This includes recording revenue such as product sales and expenses like purchasing supplies. Taking online courses can be a great way to learn the basics of accounting for your business.

If you’re a traditionalist and are more interested in tracking income and expenses than bank connectivity or cloud access, check out GnuCash. Before you can start recording any financial transactions, you’ll need to create a chart of accounts for your company. The chart of accounts is a list of accounts in your general ledger that will be used to record financial transactions.

Step 10: Run financial statements

There are numerous software options for small businesses, with QuickBooks and FreshBooks being two of the most popular. When deciding which software program to use for accounting, it helps to first consider what your business needs. You can then compare different programs to evaluate the range of features and benefits that are included, and the overall cost of using it. The IRS encourages small business owners to maintain proper documentation for expenses, such as receipts showing the amount spent, the date, the payment method, and what was purchased.

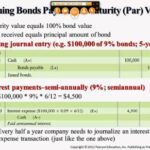

Closing Entries

Cash flow management is critical and includes forecasting how much cash you will need in the coming weeks and months. It will help you reserve enough money to pay bills, employees, and suppliers. Plus, you can make more informed business decisions about how to spend your cash. After recording transactions, you’ll want to keep copies of your invoices and all receipts. While tossing receipts in a box might seem tempting, it leads to chaos at tax time. A chart of accounts lists all business transaction and is used to compile statements, review progress and locate transactions.

There are different ways to organize files, depending on what you need to store. Minimum deposit requirements can depend on the type of business account and whether you’re opening the account at a traditional bank, credit union, or online bank. Xero starts at $9/month for the Early plan, though most small businesses will find the Growing plan, at $30/month, more suitable. FreshBooks pricing starts at $15/month for the Lite version, which is perfect for freelancers and contractors, with the option to move up to the popular Plus plan at $25/month at any time. With the help of good software, accounting for a small business can be much easier than you think. However, even if you’re only hiring an occasional contractor, you should have your payroll system set up.

small business accounting tips for business owners

Hiring a helping hand can do wonders for you, from saving you money abc technique and time doing taxes, to helping improve your chances of receiving funding and loans from investors and banks. It’s possible to hire someone part time, such as during tax season, or full time to work across all of your needs (chief financial officer, accountant and bookkeeper). Depending on your budget and the complexity of your business, costs and necessities of these will vary.

You can hire a bookkeeper, use automated accounting software, or do it yourself. Another way accounting and bookkeeping differ is that accounting is a broader field that covers a more comprehensive range of topics. As an accountant, you may be responsible for tax planning, financial statement preparation, and auditing. On the other hand, bookkeepers are typically only responsible for recording transactions and keeping track of financial data. Most of these applications cover the basics of accounting from invoicing, payments and payroll. The software can assist you in keeping accurate records and create basic financial statements.

Choose an accounting method.

- The IRS encourages small business owners to maintain proper documentation for expenses, such as receipts showing the amount spent, the date, the payment method, and what was purchased.

- Once you’ve settled on an accounting method, it’s time to set up your books.

- The Ascent, a Motley Fool service, does not cover all offers on the market.

- Be sure to download some demos and try out an application for yourself before you buy it.

Also, if you pay independent contractors $600 or more during the year, you’ll need to send each one a 1099-NEC form, how to write off a bad debt as well as copies to the IRS. The deadline for sending these forms to employees and contractors is January 31. If you have to sell inventory for a deep discount, you could deduct it from your year-end taxes. Business bank reconciliation makes it easier to discover and correct errors or omissions—either by you or the bank—in time to correct them.

Whether you choose the manual method or opt for accounting software, there are tons of accounting tools available for you to take advantage of. Another outcome of bookkeeping is being able to perform a monthly bank reconciliation. This is the process of making sure that everything you’ve recorded in your records as cash in a given month matches your bank statement, and that the total is the same. Many software solutions are available to help you speed up and partially automate the bookkeeping process, such as Intuit Quickbooks, Expensify, and Xero. As a responsible business owner, you need to record every single financial transaction you make—so the answer might depend on how many bills you pay and invoices you send out. At the very least, you’ll want to sit down for bookkeeping monthly, but we strongly recommend you update your books at least weekly, though preferably daily.

Learn how to manage your own business accounting and choose from different business accounting software. We’ll guide you through a step-by-step guide and provide resources for learning new accounting skills. The majority of your financial transactions will have to do with income and expenses. Knowing how to handle these two items will ensure that your business runs smoothly. To make your life easier, Wix allows you to create both how to void a check invoices and price quotes from your website’s dashboard so that you can collect payments from your customers in just one click. These tools will help you keep your finances organized and make it easier when it comes to tax reports and other accounting needs.