To understand how profitable a business is, many leaders look at profit margin, which measures the total amount by which revenue from sales exceeds costs. To calculate this figure, you start by looking at a traditional income statement and recategorizing all costs as fixed or variable. This is not as straightforward as it sounds, because it’s not always clear which costs fall into each category. But going through this exercise will give you valuable information. Analyzing the contribution margin helps managers make several types of decisions, from whether to add or subtract a product line to how to price a product or service to how to structure sales commissions. Before making any major business decision, you should look at other profit measures as well.

How to calculate contribution margin

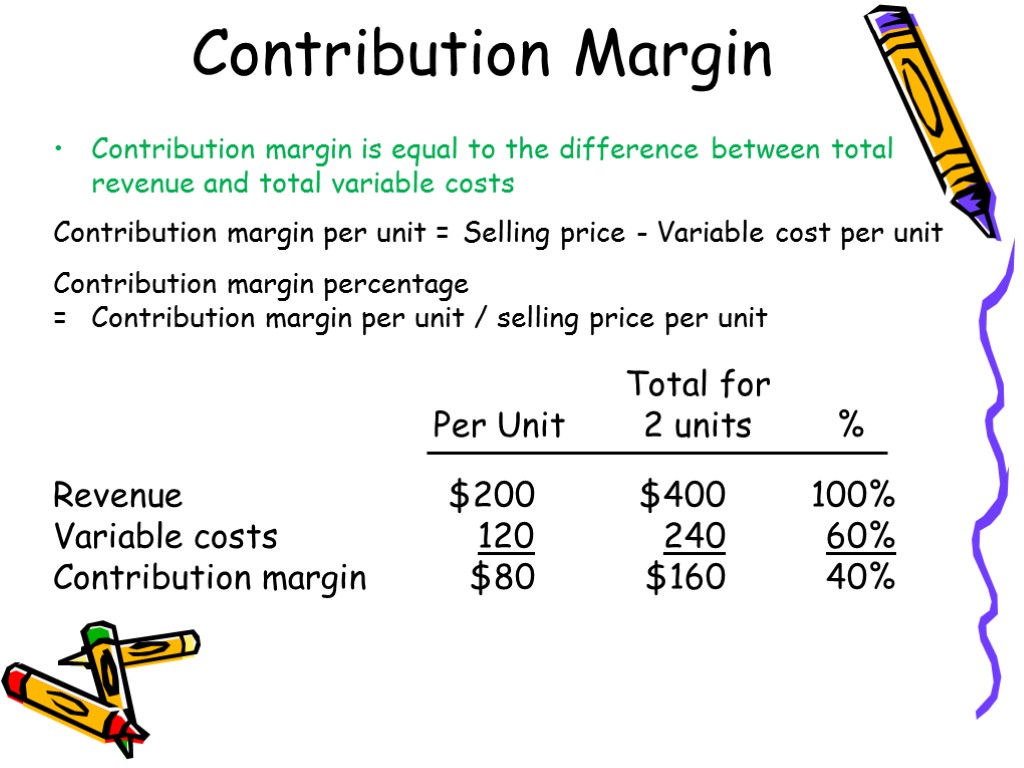

In these examples, the contribution margin per unit was calculated in dollars per unit, but another way to calculate contribution margin is as a ratio (percentage). Using this formula, the contribution margin can be calculated for total revenue or for revenue per unit. For instance, if you sell a product for $100 and the unit variable cost is $40, then using the formula, the unit contribution margin for your product is $60 ($100-$40). This $60 represents your product’s contribution to covering your fixed costs (rent, salaries, utilities) and generating a profit. This margin is a critical financial measure for businesses as it helps management make decisions regarding pricing, product mix, and resource allocation based on numbers. A higher unit contribution margin indicates that a product is more profitable and contributes more towards covering fixed costs and generating profits.

Operating Assumptions

The contribution margin is given as a currency, while the ratio is presented as a percentage. For instance, in Year 0, we use the following formula to arrive at a contribution margin of $60.00 per unit. If the contribution margin is too low, the current price point may need to be reconsidered. In such cases, the price of the product should be adjusted for the offering to be economically viable. Variable costs tend to represent expenses such as materials, shipping, and marketing, Companies can reduce these costs by identifying alternatives, such as using cheaper materials or alternative shipping providers.

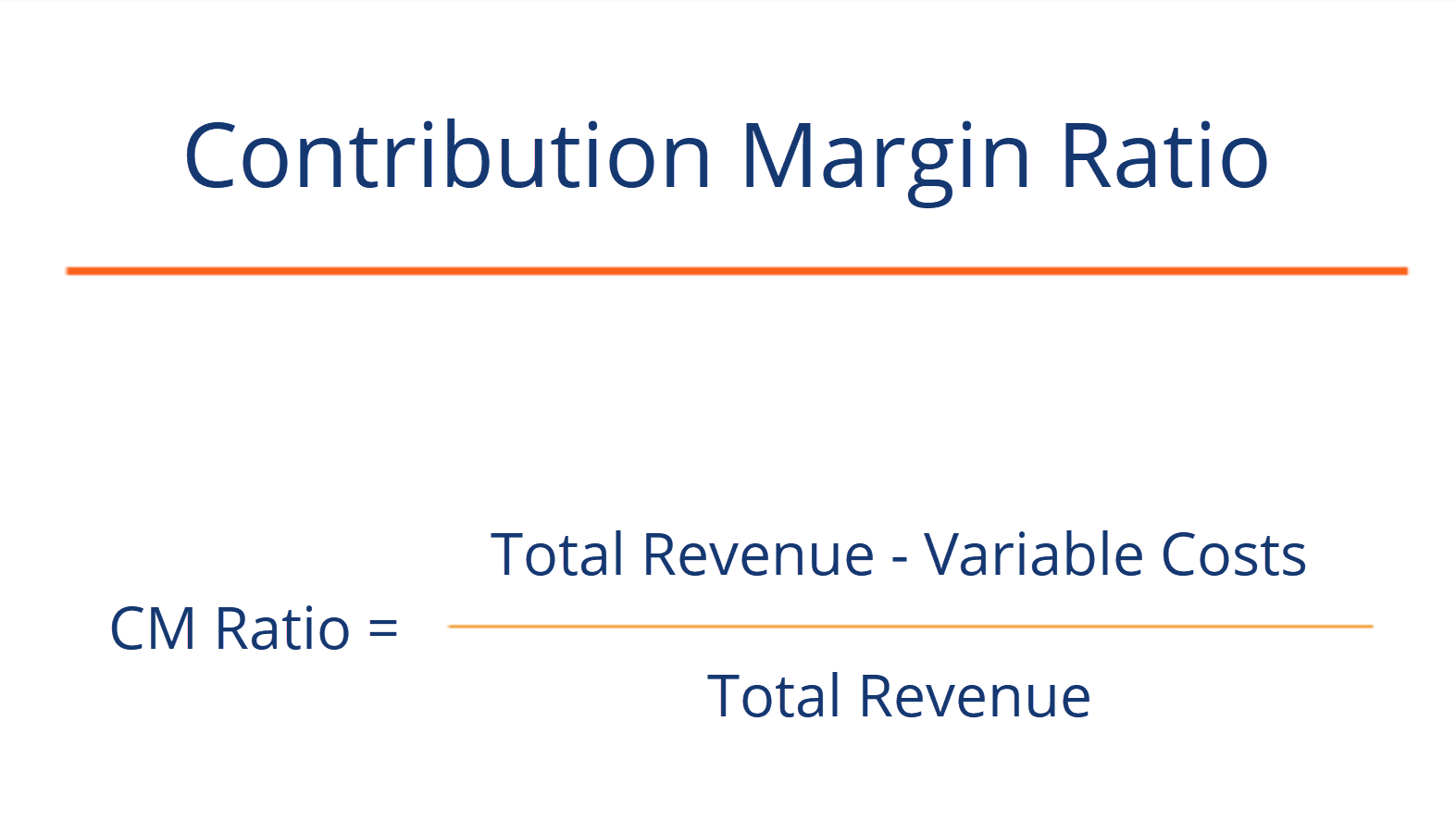

What other financial metrics are related to the Contribution Margin Ratio?

Accordingly, the Contribution Margin Per Unit of Umbrella would be as follows. Knowing how to calculate the contribution margin is an invaluable skill for managers, as using it allows for the easy computation of break-evens and target income sales. This, in turn, can help people make better decisions regarding product & service pricing, product lines, and sales commissions or bonuses. The Contribution Margin is the incremental profit earned on each unit of product sold, calculated by subtracting direct variable costs from revenue. The contribution margin shows how much additional revenue is generated by making each additional unit of a product after the company has reached the breakeven point.

Our Services

It is important to note that this unit contribution margin can be calculated either in dollars or as a percentage. To demonstrate this principle, let’s consider the costs and revenues of Hicks Manufacturing, a small 9 best accounting software for ecommerce companies best ecommerce software company that manufactures and sells birdbaths to specialty retailers. Yes, it means there is more money left over after paying variable costs for paying fixed costs and eventually contributing to profits.

- Using the provided data above, we can calculate the price per unit by dividing the total product revenue by the number of products sold.

- Some income statements report net sales as the only sales figure, while others actually report total sales and make deductions for returns and allowances.

- In effect, the process can be more difficult in comparison to a quick calculation of gross profit and the gross margin using the income statement, yet is worthwhile in terms of deriving product-level insights.

- Furthermore, it also gives you an understanding of the amount of profit you can generate after covering your fixed cost.

Total Cost

This information is useful for determining the minimum possible price at which to sell a product. In essence, never go below a contribution per unit of zero; you would otherwise lose money with every sale. The only conceivable reason for selling at a price that generates a negative contribution margin is to deny a sale to a competitor. Variable expenses directly depend upon the quantity of products produced by your company. For example, if the cost of raw materials for your business suddenly becomes pricey, then your input price will vary, and this modified input price will count as a variable cost. Say, your business manufactures 100 units of umbrellas incurring a total variable cost of $500.

Using this contribution margin format makes it easy to see the impact of changing sales volume on operating income. Fixed costs remained unchanged; however, as more units are produced and sold, more of the per-unit sales price is available to contribute to the company’s net income. The contribution margin represents how much revenue remains after all variable costs have been paid. It is the amount of income available for contributing to fixed costs and profit and is the foundation of a company’s break-even analysis.

Contribution Margin refers to the amount of money remaining to cover the fixed cost of your business. That is, it refers to the additional money that your business generates after deducting the variable costs of manufacturing your products. It is important for you to understand the concept of contribution margin. This is because the contribution margin ratio indicates the extent to which your business can cover its fixed costs. Yes, the Contribution Margin Ratio is a useful measure of profitability as it indicates how much each sale contributes to covering fixed costs and producing profits. A business can increase its Contribution Margin Ratio by reducing the cost of goods sold, increasing the selling price of products, or finding ways to reduce fixed costs.

Here, the variable costs per unit refer to all those costs incurred by the company while producing the product. These include variable manufacturing, selling, and general and administrative costs as well—for example, raw materials, labor & electricity bills. Variable costs are those costs that change as and when there is a change in the sale. An increase of 10 % in sales results in an increase of 10% in variable costs. Recall that Building Blocks of Managerial Accounting explained the characteristics of fixed and variable costs and introduced the basics of cost behavior. Let’s now apply these behaviors to the concept of contribution margin.

Therefore, the unit contribution margin (selling price per unit minus variable costs per unit) is $3.05. The company’s contribution margin of $3.05 will cover fixed costs of $2.33, contributing $0.72 to profits. For the month of April, sales from the Blue Jay Model contributed $36,000 toward fixed costs. Looking at contribution margin in total allows managers to evaluate whether a particular product is profitable and how the sales revenue from that product contributes to the overall profitability of the company.

Before making any changes to your pricing or production processes, weigh the potential costs and benefits. The contribution margin is important because it gives you a clear, quick picture of how much “bang for your buck” you’re getting on each sale. It offers insight into how your company’s products and sales fit into the bigger picture of your business. If the contribution margin for a particular product is low or negative, it’s a sign that the product isn’t helping your company make a profit and should be sold at a different price point or not at all. It’s also a helpful metric to track how sales affect profits over time.